CIBIL Myths Busted!

Learn the truth behind common CIBIL myths and improve your loan approval chances with smarter financial habits.

Talk To Loan Experts

Many people in India still believe harmful CIBIL myths that affect their loan approval chances. Understanding the truth behind credit scores can help you improve your financial profile and get better loan offers.

Whether you are applying for a home loan, business loan, personal loan, or loan against property, your credit score plays a major role in approval, eligibility, and interest rates.

What is a CIBIL Score and Why CIBIL Myths Matter?

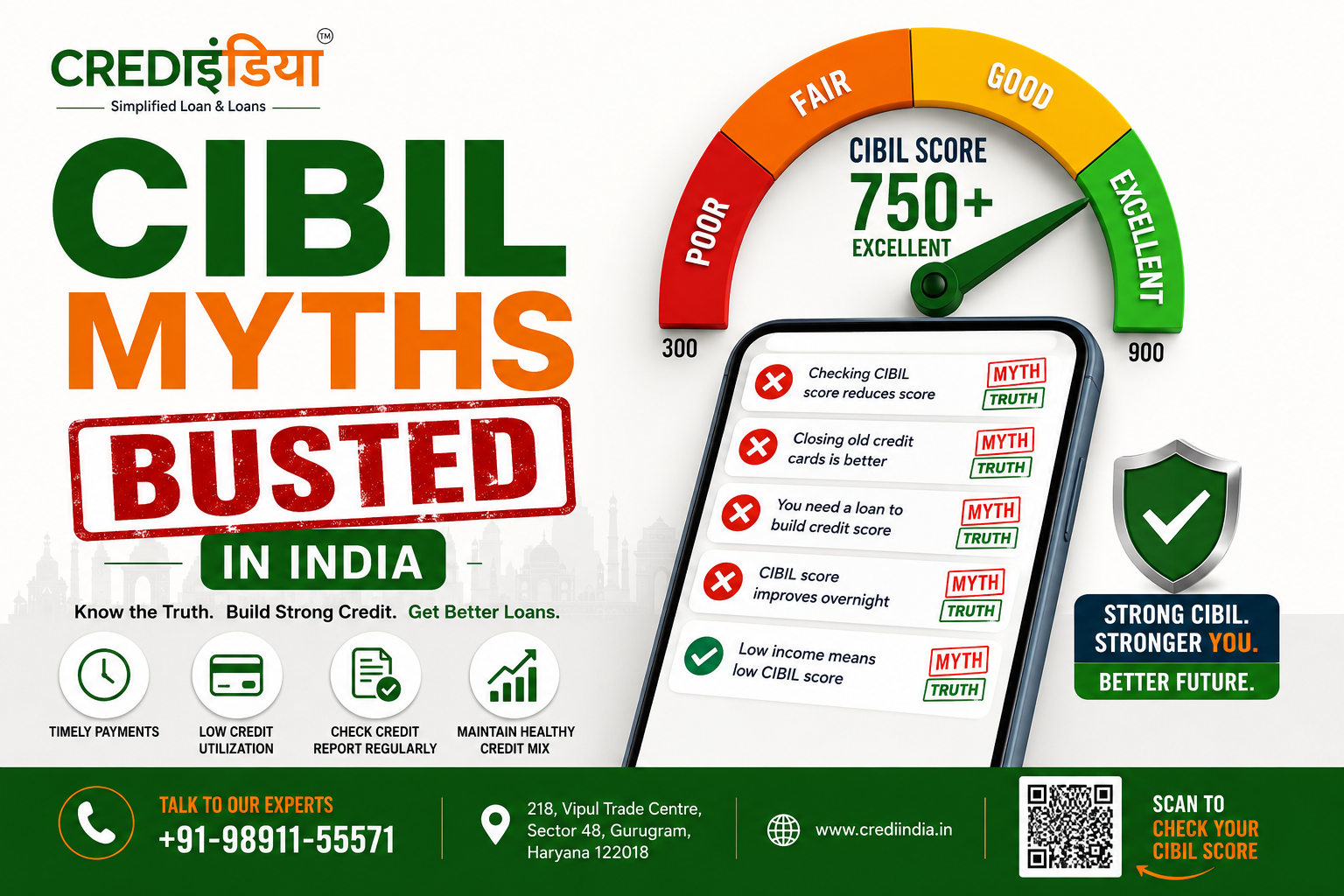

A CIBIL score is a 3-digit number ranging from 300 to 900 that reflects your repayment behaviour and financial discipline.

- 750+ = Excellent

- 700–750 = Good

- 650–700 = Average

- Below 650 = Risky

Common CIBIL Myths in India

Myth 1: Checking Your Own CIBIL Score Reduces It

Checking your own score does not reduce your CIBIL score because it is considered a soft inquiry.

Only lender checks for loan applications are counted as hard inquiries.

Myth 2: Closing Old Credit Cards Improves Score

Old credit cards improve your credit history length and positively impact your score over time.

Myth 3: You Need a Loan to Build Credit Score

Responsible credit card usage and timely bill payments can also help build a healthy credit profile.

Myth 4: CIBIL Score Improves Overnight

Improving your score takes time, consistency, and financial discipline.

Myth 5: Low Income Means Low CIBIL Score

Income and CIBIL score are different things. Financial behaviour matters more than salary level.

CIBIL Myths That Affect Loan Approval

Believing incorrect information about credit scores can reduce your chances of getting approved for loans with better interest rates.

| Myth | Reality |

|---|---|

| Checking CIBIL lowers score | Self-check does not affect score |

| Low income means low score | Credit discipline matters more |

| Closing old cards improves score | Old cards help maintain history |

How to Avoid Common CIBIL Myths

- Pay EMIs and bills on time

- Keep credit utilization below 30%

- Avoid multiple loan applications

- Maintain healthy credit mix

- Check your credit report regularly

If you are planning to apply for a Home Loan in Gurgaon, maintaining a strong credit score is extremely important.

Many borrowers also explore Business Loan Solutions for funding opportunities and expansion.

You can also check our guide on Loan Against Property to understand eligibility and approval factors.

Need Help Improving Your CIBIL Score?

Talk to CrediIndia experts and improve your loan approval chances with smart financial planning.

Check Eligibility NowFrequently Asked Questions About CIBIL Myths

Does checking CIBIL score reduce it?

No. Self-checking your CIBIL score is a soft inquiry and does not reduce your score.

What are the most common CIBIL myths in India?

Common myths include believing that checking your score lowers it, income directly affects score, and closing old cards improves credit score.

What is a good CIBIL score for home loan approval?

Most banks prefer a CIBIL score above 750 for better approval chances.

Can I get a loan with low CIBIL score?

Yes, depending on your income, collateral, repayment history, and lender policies.